Download the full submission here.

RIAA supports the use of a performance test to help safeguard the retirement savings of Australians, and notes that the current test has had the desired effect of removing a number of underperforming funds from the market.

However, the current design also leads to benchmark-hugging. It discourages long-term decision-making and can limit investment in certain asset classes, including new and emerging sectors. It reduces the sector’s ability to respond to a changing economy, including the necessary transition to net zero. Treasury’s review is therefore timely.

It is important to note that concerns around the performance test are not necessarily related to sustainability or responsible investment issues. Concerns also centre on how the test impacts investable asset classes, timing and long-term decision-making outside of climate or sustainability considerations.

There are differing views across industry, including within RIAA’s more than 500-strong member base, about whether and how the performance test should be amended. However, it is RIAA’s view that the structure and consequences of the current test acts as a regulatory barrier which, in practice, discourages investment outside a narrow set of carbon-intensive benchmarks at a time when policy settings should support the transition of the Australian economy to net zero as well as emerging tech and other crucial industries. Fund managers will increasingly need to consider and incorporate climate and non-climate-related sustainability factors into investment decision-making to remain competitive – as many already do.

Long-term investing for the purpose of providing retirement benefits is a complex proposition which interacts with the inherent complexity of the financial market. Properly measuring the value added by a trustee and ensuing trustee accountability is vital but will naturally reflect this complexity. In RIAA’s view, the options proposed in Treasury’s consultation paper only go some way to addressing the structural concerns about the performance test. Notwithstanding, we are pleased to share with Treasury the results of extensive consultations that RIAA conducted across its superannuation fund members and others that are impacted by the test. We are grateful for the strong engagement from RIAA members who contributed to this submission.

We recognise that views across industry and within our membership differ on the best path for reform.

It is RIAA’s broader view that Australia needs a joined-up, whole-of-government approach to sustainable finance. In order to facilitate investment in different asset classes, emerging sectors and in accordance with other government policy priorities, reforms to YFYS performance test must be accompanied by other policy reforms and incentives.

General comments

The performance test can be a barrier to investment decision making, but is not itself an enabler of investment

RIAA supports proportionate and pragmatic reform to the performance test. In our view, the purpose of reform should be to remove unnecessary barriers created by the current design of the test, while preserving its role as a consumer protection mechanism.

RIAA cautions against the current reform process being framed as a mechanism to direct or encourage capital toward particular sectors or to preference one investment style over another. Rather, reforms should ensure that the policy tool functions as intended and does not distort investment decision-making or create avoidable barriers for products with legitimate long-term strategies or consumer-driven objectives.

RIAA also cautions against overstating what can be achieved through (adequate) reform of the performance test. No change to the test can guarantee increased capital flows to particular sectors or broader Government priorities. Instead, reforms should seek to ensure that the test does not unduly constrain long-term investment decision-making, limit trustees’ investible universe or distort market outcomes. Where reform allows trustees to take a longer-term or more systemic view, any resulting changes in capital allocation should be understood as the operation of a better-functioning market, not as a policy failure if capital does not move in a particular direction.

As part of a whole-of-government approach, reforms to the performance test must be accompanied by other policies and incentives that encourage investment into targeted asset classes and sectors.

Having removed or improved the underperformers, the structure of the current performance test no longer properly measures underperformance of the superannuation sector. Adjustments to the test are needed to reflect distinctions and treatment of default and choice products/options. This includes accounting for the role of trustee-directed choice products, the duties of trustees, and the fact that some consumers actively choose products with different characteristics, risk profiles and timeframes.

Benchmarks set in regulation create anti-competitive market distortions and should be replaced with a more fit-for-purpose framework

RIAA considers the current benchmark framework to be a priority area for reform. Where specific benchmarks are prescribed in regulation, they can create an unhealthy gravitational pull toward a narrow set of indices and investment settings. Over time, this can entrench benchmark selection, dampen competition and innovation, and contribute to market outcomes that are less responsive to changing risks, opportunities and member needs.

This is not simply a technical design issue. With benchmarks are embedded in regulation, the performance test can operate as a market-altering tool in ways that extend beyond its intended consumer protection purpose. RIAA therefore supports moving benchmark specification and maintenance out of regulation to be administered by an independent regulatory body (such as APRA). This would provide greater flexibility and independence to ensure benchmarks remain appropriate over time, while allowing for clear thresholds, guardrails and governance arrangements to support transparency, accountability and regulatory certainty.

A framework of this kind would better support competitive and well-functioning markets, reduce unnecessary distortions in investment behaviour, reduce any perceived conflicts of interest and allow the performance test to operate more effectively as a prudential tool rather than as a blunt mechanism that shapes capital allocation through regulatory design.

The unintended consequences of the performance test may be greater for trustee-directed products, including those with certain responsible investment strategies

Trustee-directed products are a subset of Choice products, which allow consumers to take a more active role in their superannuation investment. This may include responsible investment strategies, capital preservation strategies as well as growth strategies. As APRA describes:

The choice sector enables members to have greater control of their investment strategy or to include broader services than a default MySuper product. Member choice can be a positive feature of superannuation, when choice product offerings are appropriately designed and ultimately promote the financial interest of members.1

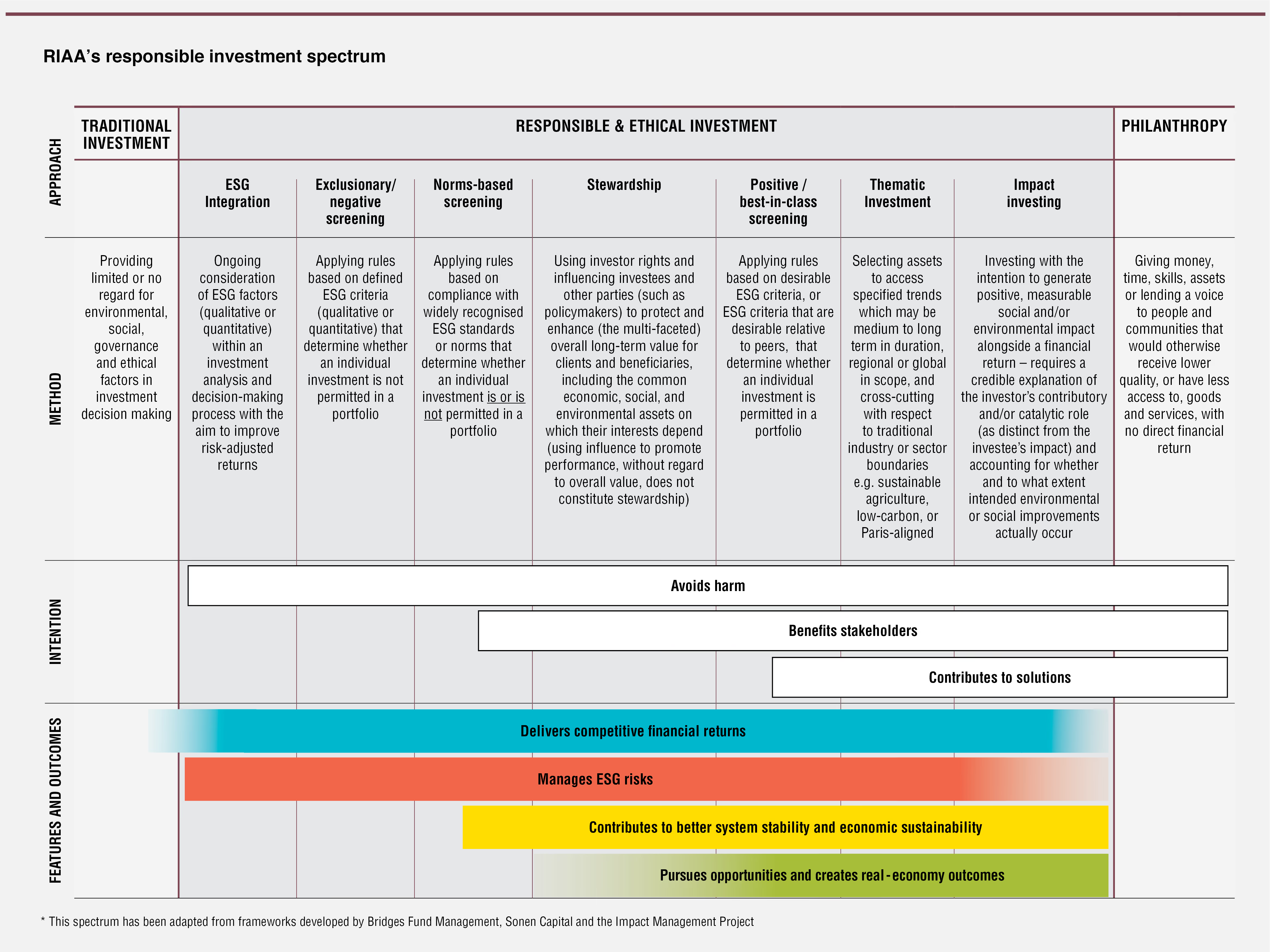

Responsible investment is a mainstream feature of the Australian superannuation and investment landscape. Most super funds use responsible investment approaches such as ESG integration and stewardship across the whole of fund as part of prudent risk management. These investment approaches improve long-term risk-adjusted returns and are not inherently inconsistent with the objectives of the performance test. RIAA would expect all super products, including MySuper products, to incorporate a degree of ESG integration.

However, the performance test may constrain long-term decision-making for strategies which have a secondary objective and go beyond traditional short-term risk and return outcomes. These are often seen in trustee-directed products. In these instances, decision-making can be constrained by:

- the carbon intensive benchmarks currently used, which do not align with the Paris Agreement or Australia’s emissions reduction targets;

- the timeframe used for the lookback period; and

- encouraging short-term decision making to pass the following year’s performance test result.

Impacts of the test are relevant for both whole-of-entity and product-specific responsible investment approaches:

- At the whole-of-entity level, the majority of funds apply ESG integration, stewardship and related practices across the full portfolio as part of prudent risk management. Some funds also employing additional responsible investment approaches such as negative screening, positive screening, and impact investing at a whole-of-entity level.

- At the product/option level, funds may also offer specific options with additional responsible investment features, such as screening, tilts or other objectives that reflect member demand. These approaches are distinct, but they can overlap within the same fund and may be affected by the same underlying structural settings of the test.

- The increased adoption of responsible investment approaches both at a whole-of-entity and product level reflect the diversity of approaches and options available within the market to cater to investment needs and preferences.

Features such as negative screening, positive screening or other approaches used in the investment strategy and shaped by member demand can increase tracking error against the prescribed benchmarks or create a mismatch between the product’s long-term investment approach and the shorter-term performance settings of the test. At the same time, whole-of-entity approaches may also be affected where benchmark design narrows the investable universe or discourages long-term positioning.

For this reason, RIAA considers unintended consequences for some investment strategies to be a subset of a broader structural issue within the current test design, which is misaligned with the objective of the performance test. Reform should focus on addressing this structural mismatch in a way that better reflects differences between product types, trustee duties and consumer choice, while recognising the overlap between whole-of-fund responsible investment practices and more specific product-level strategies.

Reforms should be fit for long-term investments and respect consumer choice

The timeframes in the current performance test are inconsistent with so-called "non-traditional" assets such as many sustainability-related assets. RIAA contends that despite the Government extending the performance test lookback from 8 years to 10 years in 2023, aspects of the performance test will remain challenging while the formulation of the benchmark continues to limit investors’ ability to deviate in search of longer-term outcomes.

Additionally, it is important to ensure performance benchmarks are established in a manner that allows superannuation funds to invest consistent with delivering strong, long term investment returns, aligned to the time horizons of their beneficiaries. There are significant differences between the views of older and younger Australians. For example, RIAA’s 2022 consumer research3 found that different generations responded very differently to the question of whether they would be more motivated to try to save more if their savings and investments made a positive difference in the world:

- Gen Z: 83%

- Millennials: 75%

- Gen X: 57%

- Baby Boomers: 39%

We note that some Gen Z superannuation fund members today will retire in the 2070s, and that this cohort and time horizon should be considered significant when viewing the systemic risks of poor longer-term performance of unsustainable assets.

There is a greater diversity of offerings of responsible investment approaches in trustee-directed products where consumers make an active decision to choose their preferred product. These include some sustainable-labelled and faith-based options, as well as some with different risk profiles and longer-term objectives. By not recognising the deliberate choice of consumers to follow a particular investment strategy, in many cases informed by their specific values, the performance test may fail products that are in fact delivering on members’ investment choices or consistent with their specific beliefs, as well as delivering on financial return. This is contrary to the Government’s objective for the performance test which includes improving member outcomes.

It is important to note that trustee-directed products are a diverse mix, and include single asset classes, and smaller ethical funds, and that any assessment of their performance should be understood in relation to the specific focus of the product, the objectives of the members, and the particular exclusions that could be a factor in driving any tracking error.

Superannuation fund members increasingly expect their money to be invested in line with their own values, in addition to returning strong financial returns. RIAA’s study, From Values to Riches 2024: Charting consumer demand for responsible investing in Australia found high expectations that funds will invest responsibly: 88% of Australians expect their bank account and their super to be invested responsibly and ethically.

Consider other policy levers within the performance test to address structural impediments

RIAA supports efforts to reform the performance test. However, the options considered in this consultation appear unlikely, on their own, to fully address the structural issues the review is seeking to resolve.

For that reason, RIAA encourages the Government to consider other policy levers within the performance test as a future focus for reform. We make this point at a high level only, noting that these matters are not the focus of the current consultation and may require further policy development and consultation.

Consider recalibrating the consequences of failing the test

The original purpose of the test was to protect members from sustained underperformance through transparency and direct consequences upon failure. That objective remains important. At the same time, there may be scope to consider whether the current consequences to failing the test remain the most proportionate and effective way to achieve that purpose across a broader and more diverse set of products.

RIAA suggests that targeted adjustments to the consequences of failing the performance test (not removing accountability and consequences altogether) may, where carefully designed, support the effectiveness of the test as a consumer protection tool by helping ensure it continues to operate as intended in an evolving superannuation landscape. This would not weaken the test itself, as accountability would continue to be paramount. Depending on design, recalibration could instead improve alignment between the test’s operation and its original policy intent.

The initial policy and regulatory attention for the performance test was on default products and the introduction to Choice products was deferred an additional year, acknowledging that it was important “to ensure the test is fit for purpose given the significant variety and complexity of [non-Choice] products."4 However, the current consequences of failing the test, including member notifications in the first year and prohibiting new members in the second year, were not reviewed or evaluated for appropriateness when the test was extended to trustee-directed products. As the test extends to a broader range of trustee-directed products, it is reasonable to consider whether a uniform approach to consequences remains appropriate in all cases.

Consumers must actively select their superannuation to be with a trustee-directed product/option with higher growth exposures, longer investment horizons or more specific strategies. For example, a member may deliberately choose a trustee-directed high-growth option with an eight-year or longer recommended investment horizon, accepting greater short-term volatility in pursuit of stronger long-term returns. In that context, automatic closure to new members after only two years of relative underperformance (where the metric used to measure performance may not be relevant) may not always align neatly with member choice or product design, particularly where such consequences were originally developed with default products in mind. There may be merit in considering whether consequences should operate differently across Default and Choice arrangements, while maintaining accountability for all products that underperform.

Consider the role of fees within the performance test

We note that the current consultation does not address the treatment of fees despite fees forming a significant component of the performance test formula. Yet while the performance calculation spans a multi-year period, the current approach effectively captures only a single-year snapshot of administration fees.

We recognise that expanding reform to fees and consequences would add complexity to an already difficult policy area. However, to address structural distortions in investment behaviour, further work may ultimately be needed across all of the key settings that shape those incentives. In particular, if the current consequences are a significant driver of the behaviours this consultation is seeking to address, there may be limits to how far benchmark-focused reform alone can resolve those concerns. This reinforces the case for keeping broader structural settings under review, even if they are not considered as part of this consultation.

'Download submission' for responses to consultation questions.

1APRA Information Paper (2021), Choice sector performance: improving outcomes for superannuation members

3RIAA Consumer Research, From Values to Riches 2022: Charting consumer demand for responsible investing in Australia

4Australian Treasury (2022) Review to strengthen super | Treasury Ministers