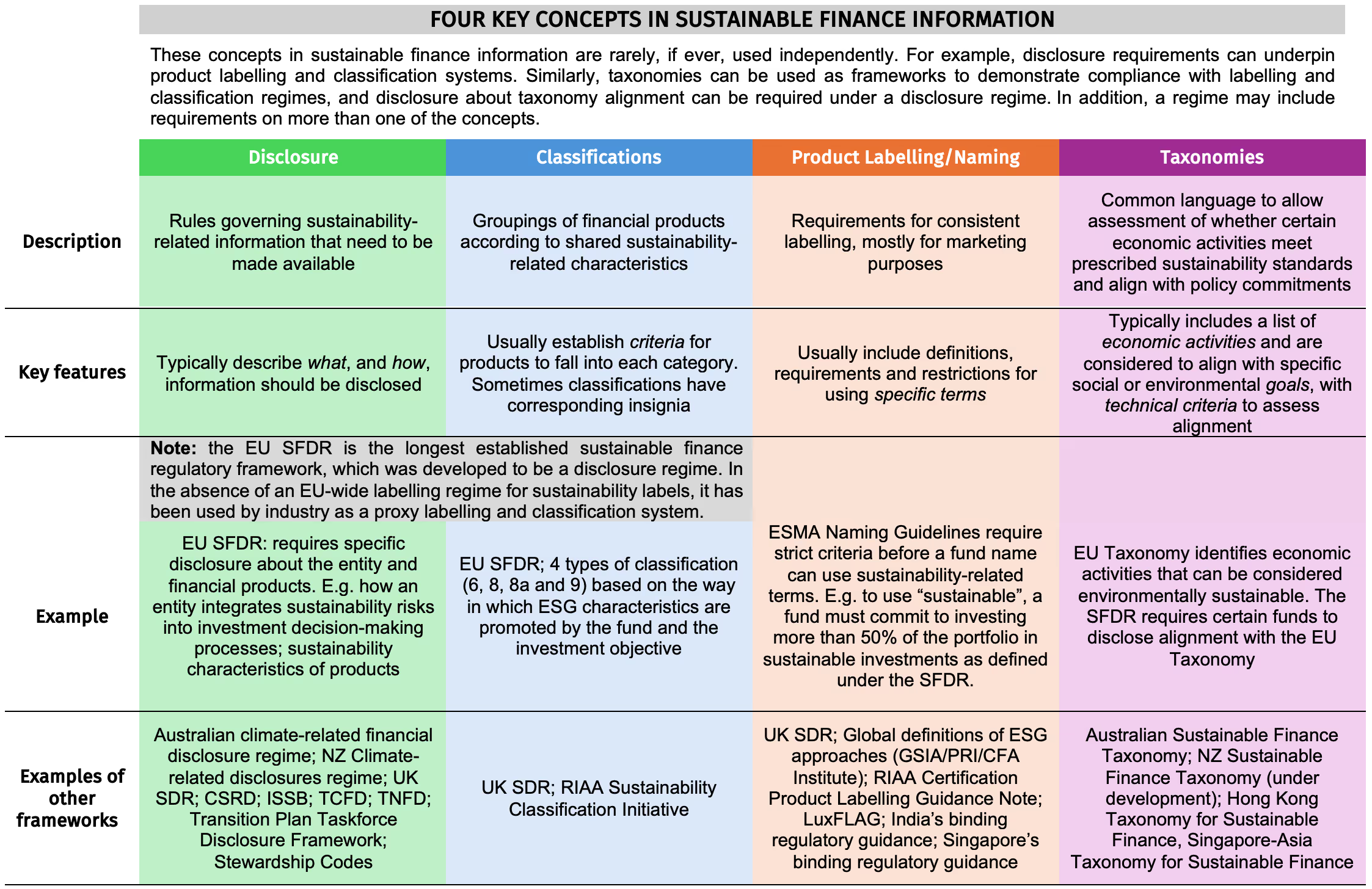

Information and transparency are vital for informed consumers, quality products and strong market integrity. To assist with comprehension and application, there are different ways of organising this information.

For sustainable finance, there are four key concepts when it comes to information about financial products:

· product disclosure requirements

· product classification systems

· product labelling or naming regimes and

· taxonomies.

These concepts can be interdependent and reinforce each other, for example:

- Product disclosure enables transparency about taxonomy alignment, product classification, and product labelling.

- Taxonomies can provide the foundation for product classification and product labelling regimes.

- Product labelling and product classification help consumers and investors navigate the market confidently.

Together, they create a coherent framework that supports sustainable investment, regulatory oversight, and market integrity.

Four key concepts in sustainable finance product information

RIAA Certification

Disclosure Requirements

Building Transparency in Sustainable Finance – Disclosure requirements are the backbone of sustainable finance. They ensure that financial institutions openly share how their investment products address environmental, social, and governance (ESG) factors.

Why It Matters:

· Transparency: Investors and stakeholders gain insight into how sustainability risks and opportunities are managed.

· Accountability: Institutions are held responsible for their sustainability claims and practices.

· Comparability: Standardised disclosures make it easier to compare products and entities across markets.

Key Features

Typically describe what, and how, information should be disclosed

Example

The EU Sustainable Finance Disclosure Regulation (SFDR) mandates that financial entities disclose how they integrate sustainability risks into investment decisions and the sustainability characteristics of their products.

RIAA Certification example

The RI Certification Standard imposes disclosure requirements for financial products seeking certification. It requires certified product providers to:

Have formal, consistent, documented, and auditable RI strategies and processes:

RI Strategies:

a. are fully explained in legal product documentation such as the Product Disclosure Statement (retail), Information Memorandum or Pitch book (wholesale) and/or equivalent documentation that supports the product, and

b. are consistently and reliably represented between the legal documentation, supplementary materials, website and other public platforms… (P1)

For additional information on how this is applied in practice see: Verification - Product and service certification

Examples of other frameworks

UK Sustainability Disclosure Requirements (SDR); New Zealand climate-related disclosures (CRD) regime; EU Corporate Sustainability Reporting Directive (CSRD); IFRS Sustainability Disclosure Standards by the International Sustainability Standards Board (ISSB); Task Force on Climate-related Financial Disclosures (TCFD); Taskforce on Nature-related Financial Disclosures (TNFD); Transition Plan Taskforce (TPT) Disclosure Framework; Stewardship Codes

Classifications Systems

Helping Investors Navigate the ESG Landscape – Classification systems group financial products based on shared sustainability characteristics. They provide structure and clarity in a rapidly evolving market.

Why It Matters:

- Investor Clarity: Helps consumers and investors identify products that align with their values and sustainability goals.

- Market Efficiency: Reduces confusion and enhances confidence in ESG-labelled products.

- Policy Alignment: Supports regulatory efforts to direct capital toward sustainable activities.

Key Features

Usually establish criteria for products to fall into each category. Sometimes labels have corresponding insignia.

Example

Under the EU Sustainable Finance Disclosure Regulation (SFDR), funds are classified into categories (e.g., Article 6, 8, and 9) based on how they promote ESG characteristics or pursue sustainable investment objectives.

Note: the EU SFDR is the longest established sustainable finance regulatory framework, which was developed to be a disclosure regime. In the absence of an EU-wide labelling regime for sustainability labels, it has been used by industry as a proxy labelling and classification system.

RIAA Certification example

The RI Certification Standard is not itself a classification system, however, adherence to the RI Certification Standard is a pre-requisite for a RIAA Sustainability Classification. The RIAA Sustainability Classifications Initiative assigns three classifications:

· Responsible

· Sustainable

· Sustainable Plus.

These classifications differentiate RIAA certified products based on their responsible investment approaches, claims, processes, stewardship programs and disclosures. They focus on the approach taken in considering ESG factors and the degree to which sustainability is addressed or targeted.

Sustainability classifications webpage

Examples of other frameworks

UK Sustainability Disclosure Requirements (SDR)

Product Labelling/Naming Regimes

Ensuring Integrity in Sustainability Marketing – Product labelling or naming regimes set rules for how sustainability-related terms can be used in product names and marketing materials. They protect consumers from misleading claims and promote trust.

Why It Matters:

· Greenwashing mitigation: Labels can only be used if specific criteria relating to sustainability are met.

· Consumer protection: Ensures that sustainability claims reflect the nature of the financial product and therefore not misleading consumers.

· Global consistency: Harmonised labelling supports investment across international borders and regulatory certainty.

Key Features

Usually include definitions, requirements and restrictions for using specific terms.

Example

The ESMA Naming Guidelines require strict criteria before a fund name can use sustainability-related terms. For example, to use the term “sustainable”, a fund must commit to investing more than 50% of the portfolio in sustainable investments as defined under the EU Sustainable Finance Disclosure Regulation (SFDR).

RIAA Certification example

The requirement to ensure that responsible investment labels are clear, honest and not misleading is one of eight criteria that comprise the RI Certification Standard. Product providers are required to:

Make honest claims and are appropriately labelled:

a. are named to accurately reflect the claims pertaining to social, environmental, sustainability and/or ethical outcomes or responsible investment approach applied to the product; and

b. describe what could be reasonably expected by an investor in terms of the portfolio holdings of the product; and

c. ensure all claims made about the product are honest and not false or misleading nor include puffery, un-substantiations and unqualified predictions. (P2)

Have relevant and accessible RI disclosures:

for products asserting certain sustainability outcomes or claims, publish the product’s social, environmental and/or sustainability performance against benchmarks, goals or targets, at least annually as well as the methodology for measuring the Product’s contribution to social, environmental and/or sustainability outcomes. (P5e)

The Product Labelling Guidance Note includes additional information on these requirements, such as requiring that:

Products with climate-related labels should prominently disclose the proportion of underlying investments that align with their label including an explanation of how that proportion has been measured. This includes the basis for determining what classifies as their label definitions, e.g. data provider classification, taxonomy, or proprietary methodology.

Examples of other frameworks

UK Sustainability Disclosure Requirements (SDR); Global definitions of ESG approaches (GSIA/PRI/CFA Institute); India’s binding regulatory guidance ‘New category of Mutual Fund schemes for ESG Investing and related disclosures by Mutual Funds’, LuxFLAG; Singapore’s binding regulatory guidance ‘Disclosure and Reporting Guidelines for Retail ESG Funds’

Taxonomies

Creating a common language – Taxonomies are structured frameworks that that allow assessment of whether certain economic activities (usually assets, projects, facilities or measures) meet prescribed sustainability standards and align with policy commitments.

Why It Matters:

· Clarity & Consistency: Helps investors and regulators understand what qualifies as sustainable.

· Policy Support: Aligns financial flows with national and global sustainability goals.

· Credibility: Technical criteria ensure that sustainability claims are measurable and verifiable.

Key Features

Typically includes a list of economic activities and are considered to align with specific social or environmental goals, with technical criteria to assess alignment.

Example

The EU Taxonomy identifies economic activities that can be considered environmentally sustainable. The SFDR requires certain funds to disclose alignment with the EU Taxonomy.

RIAA Certification example

While the RI Certification Standard is not itself a taxonomy, nor does it explicitly reference taxonomies, guidance notes on specific areas outline how a taxonomy may be used by a product provider to adhere to the Standard.

For example, to meet the product labelling requirements of the RI Certification Standard, the Product Labelling Guidance Note provides that climate-related claims of a product should not contradict any other claims or practices of the product and that any perceived contradictions should be clearly explained. As part of this explanation a product provider may use “a clear definition of what qualifies as a climate solution, for example, through the use of a particular taxonomy…”.

Examples of other frameworks

Australian Sustainable Finance Taxonomy; NZ Sustainable Finance Taxonomy (under development); Hong Kong Taxonomy for Sustainable Finance, Singapore-Asia Taxonomy for Sustainable Finance